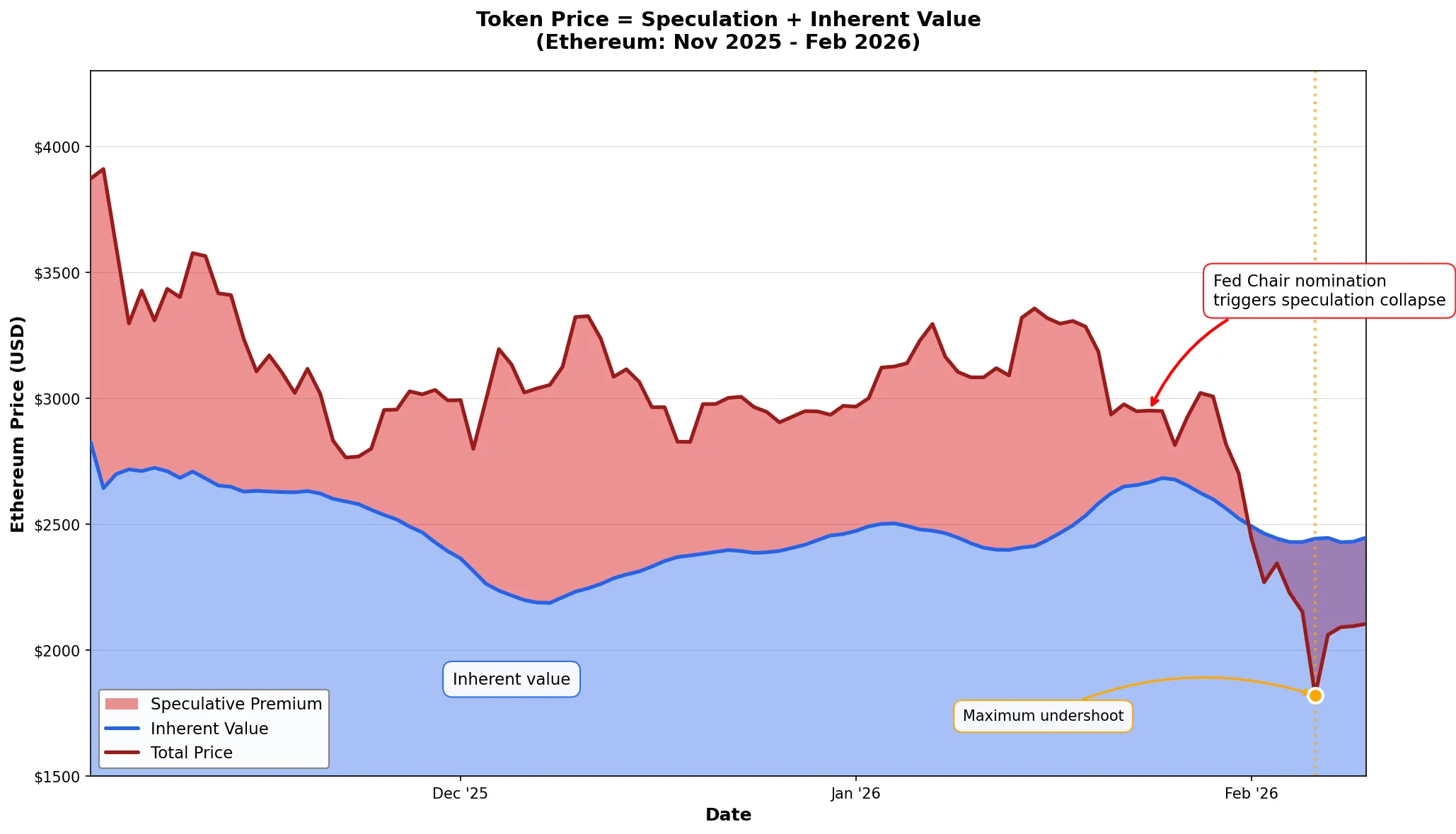

What actually happened during the Crash

The selloff had a pattern. Kevin Warsh’s Fed nomination triggered a flight from risk assets. Gold dropped . Silver absolutely cratered at . Bitcoin and Ethereum followed because they trade like risk assets now. That part’s not surprising.

But this is my favourite part: the crash had a floor.

Bitcoin didn’t stay below $. Ethereum found support around $. And when Bitcoin ETFs were bleeding $ billion in outflows but prices stabilized anyway? That’s when I started paying attention differently. The market was basically saying “Okay, the speculation premium is toast, but there’s still something here worth this much.”

I kept asking myself: what actually changed about these networks during the crash?

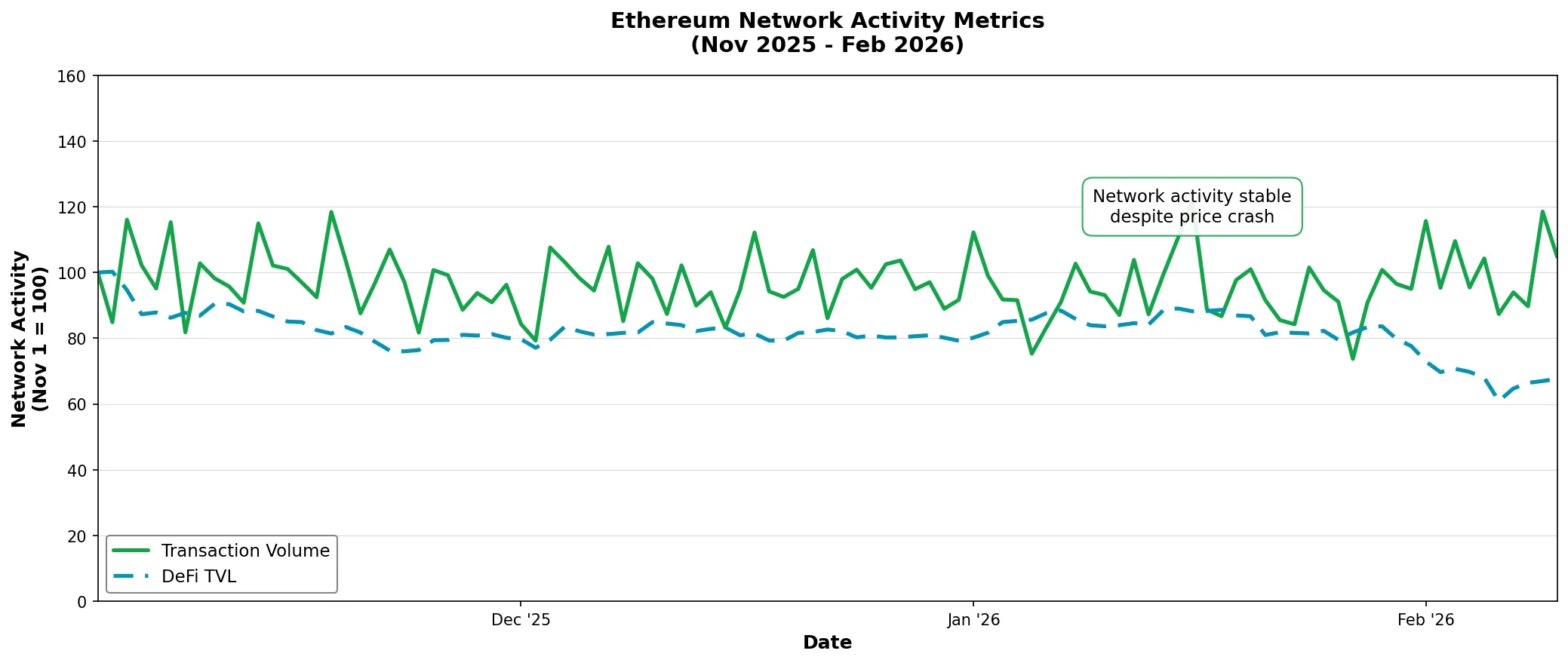

- Did Ethereum stop processing DeFi transactions? No.

- Are smart contracts broken? No.

- Did Chainlink’s data feeds stop working? No.

The infrastructure kept humming along while prices imploded - Uniswap processed $ billion in trading volume in January 2026. Aave had $ billion in total value locked. These aren’t hypothetical use cases — these are actual businesses running on blockchain infrastructure, generating real fees, serving real users. The crash didn’t change those numbers meaningfully.

That’s the distinction I’m talking about.

- Speculation responds to Fed appointments and regulatory headlines: it’s all forward-looking sentiment and fear.

- Inherent value comes from the network actually doing something useful: Processing transactions, securing assets, enabling applications people pay to use.

Here’s an analogy that clicked for me: think about Chase credit card points. They’re valuable because you can convert them to actual services — flights, hotels, whatever. But their value doesn’t swing wildly because you can’t trade them. There’s no speculation layer on top.

Crypto tokens are weird because they’re both things at once. They’re the unit you need to access network services (like Chase points) and they’re publicly tradable assets (like stocks). So their price reflects what the network provides today plus what traders think it might provide in five years. When that second part gets violently repriced, people see the total price drop and assume the first part collapsed too.

It didn’t. The networks kept running.

The Key Difference: Credit card points aren’t tradable = no speculation layer. Crypto tokens are tradable = speculation + utility bundled together. When speculation crashes, people assume utility crashed too. It usually didn’t.

Here’s Where This Gets Uncomfortable

If inherent value is so real and measurable, why can’t anyone agree on what it actually is? Why does “smart money recognizing value at $” look identical to “sellers just got exhausted” to everyone else?

The honest truth? We’ve built the most transparent financial system in history, and somehow made it impossible to understand.

That’s DeFi’s big paradox. Everything’s on-chain. You can verify every transaction, audit every smart contract, trace every token movement. Perfect transparency. But then you try explaining to a traditional finance person what’s actually happening, and you’re drowning them in jargon—Layer 1 protocols, cross-chain bridges, automated market makers, yield farming strategies.

Behind all that complexity is actually a simple phenomenon: these networks are useful infrastructure that people pay to use, and tokens quantify access to that infrastructure. That’s it. But we’ve wrapped it in so much technical language that most finance professionals — smart people who understand complex systems — can’t tell what’s real utility and what’s speculation.

So when prices crash, they assume it was all speculation because they never understood the utility in the first place.

If the market can’t distinguish these components, does this distinction even matter? Maybe inherent value is just something we “believers” tell ourselves after crashes to feel better.

But here’s the thing: Every technology goes through this exact cycle. Early internet stocks were insanely volatile. Most crashed and disappeared. But the ones with real utility — Google, Amazon, Microsoft — survived the volatility and eventually got valued on their actual business fundamentals more than hype.

The difference is comprehension. Today, you can explain cloud computing or e-commerce to any CFO and they’ll get it. They can evaluate fundamentals. That comprehension reduces the speculation premium.

Crypto’s not there yet. Fifteen years isn’t nearly enough. Regulatory uncertainty makes it worse. Most institutional investors — and I mean smart people running billions — still don’t fully understand what they’re buying beyond “digital asset with high volatility.”

That’s why speculation dominates.

Even With All That Uncertainty, Here’s Why I Still Care

The volatility isn’t going away anytime soon. Regulatory headlines will keep triggering moves. Speculative traders aren’t disappearing.

But understanding this dual-value framework completely changed how I interpret these swings.

When Ethereum dropped , my gut reaction was panic — that’s brutal. But then I did what you’d do with any other asset: checked the fundamentals. Transaction volumes barely moved. DeFi protocols kept functioning. The actual network activity that generates value continued almost unchanged.

The speculation got repriced. The utility kept running.

This matters if you’re trying to figure out whether blockchain technology has legs beyond trading. Market crashes are noise. What actually matters is: are these networks solving real problems? Are people willing to pay to use them? Is the technology improving?

The answers are yes, yes, and yes — even after the crash.

I can’t tell you where to buy or when speculation bottoms out. I can’t tell you if $70,000 Bitcoin was cheap, fair, or still overpriced. I don’t know. The market’s still figuring that out, and honestly it might take years.

But the distinction between speculation and utility is real, even if the market’s terrible at pricing it cleanly. And as regulatory clarity comes, as institutional understanding deepens, as more people actually comprehend what’s happening under the hood, the speculative premium will moderate. Not disappear.

If You’re Still With Me, Here’s What I Think We Should Do

Stop obsessing over price charts for a minute. I know that’s hard when volatility is this crazy, but hear me out.

Look at usage metrics instead. Transaction volumes. Number of applications being built. Real economic activity happening on these networks. Those metrics persisted through the crash. That’s the signal beneath all the noise.

The crash validated something important: there’s a layer of actual utility that survives panic selling. That’s what we should be evaluating.

I could be completely wrong if we never achieve the comprehension breakthrough. If blockchain complexity stays impenetrable, if regulation kills innovation, if something better comes along — then inherent value stays theoretical forever and speculation wins.

But I’m betting against it. The transparency is there. The utility is there. We just need to build understandability on top of it. And honestly? We should be leading that translation effort, not leaving it to the conspiracy-theorist parts of crypto Twitter.

When we figure out how to explain this stuff clearly — when “blockchain infrastructure” becomes as comprehensible as “cloud computing” — token prices will still fluctuate. But the conversation shifts from “is this a scam?” to “which networks deliver the most value per dollar?”

The infrastructure’s still here. The networks still work. And if you understand that distinction, you’re already ahead of most people panicking over price charts.

That’s what the crash taught me, anyway. Your mileage may vary.