Why DCF Still Works: The Fundamental Structure Holds

I believe the core DCF logic is completely unshaken in crypto. Take Ethereum. Each transaction pays a gas fee: a real charge for computational resources. Users pay these fees willingly because the network provides utility. As adoption grows, transaction volume increases. As volume increases, revenue rises. This is the exact same relationship we’d find in Visa’s payment processing business:

The structural components translate directly. Free cash flow to the firm becomes protocol fee revenue minus operating expenses. Terminal value follows similar logic. WACC must account for regulatory and technology obsolescence risk, but this is conceptually identical to adjusting WACC for a fintech startup in an evolving regulatory environment.

Here’s the critical insight: we’re valuing the company’s equity, not the token itself. The token derives value from network utility—users’ willingness to pay for protocol services. The company equity represents ownership of corporate assets, including cash, IP, and crucially, any token reserves on the balance sheet. These are related but distinct instruments with completely different value drivers.

Let me address the obvious objection: “If tokens and equity are separate, why does token price correlate so strongly with company valuation?” Fair enough. The correlation exists because token performance affects the company’s balance sheet—when token reserves appreciate, company assets increase. But the causation runs from network adoption to token value, to company asset value. Not from company operations to token value.

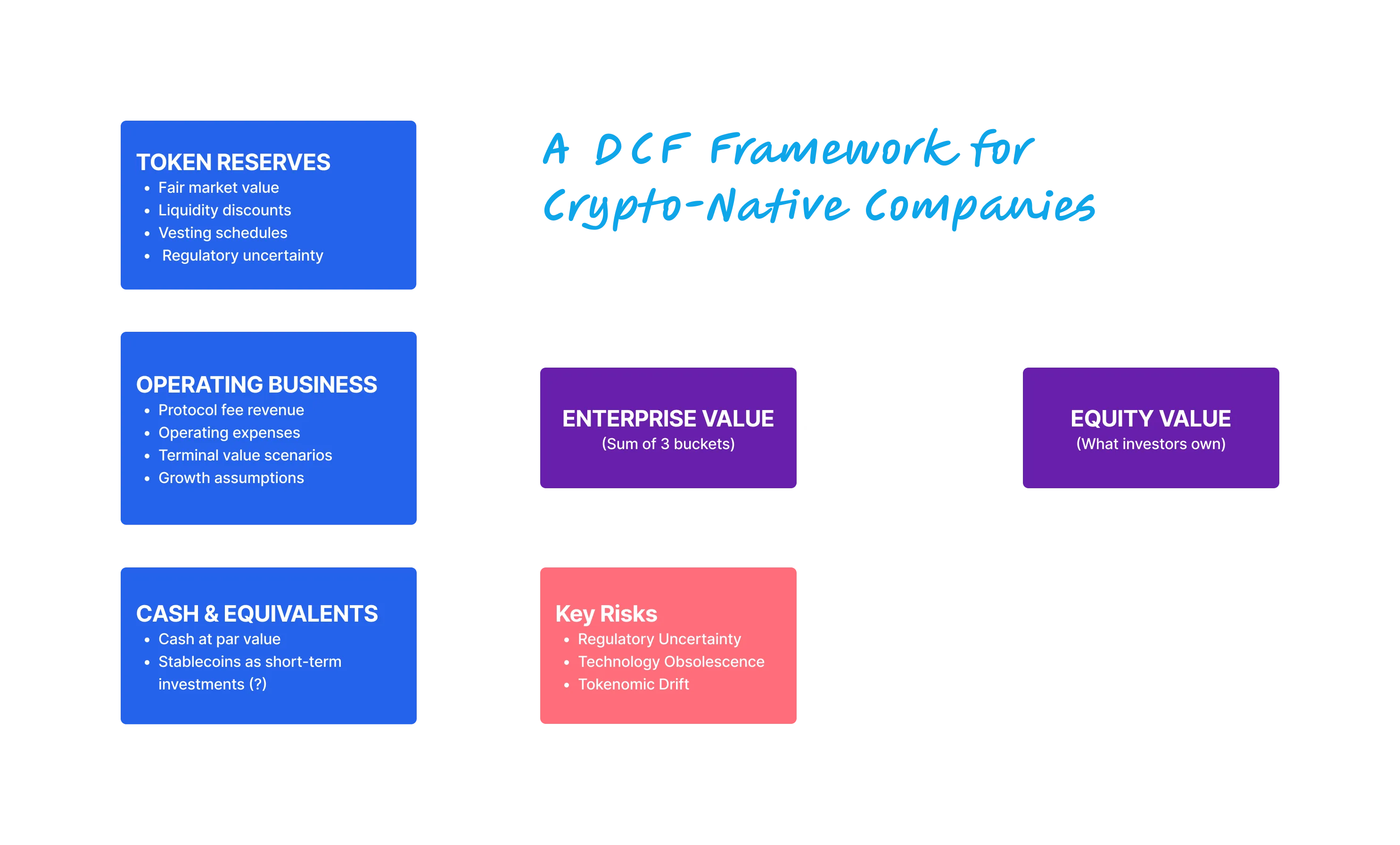

The Token Reserve Puzzle: Not Treasury Stock, But Liquid Assets

The single most important mental shift required here, and the one that tripped me up for months: is understanding how to treat tokens held by the issuing company. Our instinct, trained on traditional finance, screams “treasury stock.” Treasury stock doesn’t appear as an asset on the balance sheet; it reduces equity in shareholders’ equity. We can’t pay dividends to ourself or meaningfully vote our own shares.

Crypto company token reserves work completely differently. They do appear as assets because they represent genuine, separable economic value. These tokens derive value from network effects and protocol utility, not from claims on the company’s cash flows. An Ethereum token’s value comes from users’ demand for computational resources on the Ethereum network. The Ethereum Foundation holds roughly of total ETH supply, but these tokens don’t give the Foundation a claim on its own operational cash flows. They’re assets whose value fluctuates based on network adoption, security, and utility to the broader ecosystem.

Think of it this way: A restaurant chain holding gift cards to its own restaurants accounts for those as liabilities (obligations to provide future meals). But a restaurant chain holding shares in a separate cooperative that processes all restaurant payments would account for those shares as investments. The restaurant doesn’t control the cooperative’s value drivers—network effects among all participating restaurants do. Crypto company token reserves are the latter case.

This distinction has massive valuation implications. We need sum-of-the-parts (SOTP) methodology. I break it into three buckets:

-

Cash and cash equivalents: Straightforward present value. Though I’ll admit, there’s an unresolved question about whether certain stablecoins should be treated as cash equivalents—the SEC and FASB are still figuring this out. For now, I classify stablecoins as short-term investments rather than cash equivalents, but this could change.

-

Operating business value: This is where our core DCF lives. Project future protocol fees, subtract operating expenses, calculate free cash flow, discount to present value. This captures the value of technology infrastructure, developer talent, and the company’s ability to generate future fee revenue.

-

Token reserves: Mark these to fair market value for liquid tokens, with appropriate discounts for lockup periods or vesting schedules. For illiquid tokens, we can use recent private transaction prices or comparable protocol valuations. The FASB’s 2023 guidance (ASU 2023-8) requires crypto assets to be reported at fair value even without active markets, which actually helps standardize this approach.

The SOTP approach reveals potential mispricings. Consider Ripple. Ripple Labs holds approximately 46 billion XRP tokens. With $ billion in cash and XRP trading at $, the theoretical asset value would be roughly $ billion. Yet secondary market equity transactions implied company valuations of $ billion to $ billion—discounts of to relative to asset value. These discounts reflect liquidity constraints on equity, regulatory uncertainty (the SEC lawsuit), and the market’s assessment that Ripple may not realize full value from its holdings. Using SOTP, we explicitly quantify each of these factors rather than accepting the discount as some unknowable market mystery.

I’m treating these discounts as purely rational market assessments of specific risks. But honestly? Sometimes these discounts reflect pure market inefficiency or lack of sophisticated buyers in secondary markets. I could be completely wrong if private equity firms with deep crypto expertise start aggressively bidding up these discounted equity positions. That hasn’t happened yet at scale, which makes me think the discounts are at least partially justified (but I’m watching for this).

The Mechanics

Translating Crypto-Centric Revenue Models Into DCF Terms

Revenue forecasting for crypto protocols requires translating blockchain-native business models into DCF language. The good news: most successful crypto revenue models have direct traditional finance analogues. The challenge is modeling adoption dynamics.

Transaction Fee Protocols

Transaction fee protocols are the most straightforward. These include decentralized exchanges (Uniswap), layer-1 blockchains (Ethereum, Solana), and payment networks (Ripple). Revenue equals transaction volume times fee rate. Uniswap charges on trades, generating $ million in fees over the past year. A portion goes to liquidity providers, the remainder is protocol revenue. To forecast this, we model transaction volume growth and fee rates.

Bottoms-Up: Build transaction volume from granular drivers. For a decentralized exchange: number of active traders, average trades per user per month, average trade size, fee percentage. Each component gets its own growth assumption. If we project active users in Year 1 growing annually, with trades per month averaging $, at fees, we forecast:

in Year 1 revenue. The advantage is granularity: we can stress-test user growth separately from trading frequency.

Top-down: This starts with total addressable market. Estimate global DeFi trading volume ($ trillion annually), assume our addressable market is ($ billion), project market share ($ billion), apply the fee rate to get $ million in revenue. Top-down works for early-stage protocols without user history, or when creating scenarios tied to macro crypto adoption.

Lending Protocols

Lending protocols (Aave, Compound) generate revenue by capturing the spread between borrowing and lending rates. Borrowers pay interest, lenders receive most of it, the protocol captures a small percentage (often basis points). We need to model total value locked (TVL) in lending pools, utilization rates (percentage of deposited assets actively borrowed), interest rate curves, and the protocol’s take rate. Simplified: $ billion TVL, utilization, average borrowing rate, basis point protocol take yields:

on an annual basis. As TVL grows, revenue scales proportionally.

The Discount Rate Problem: WACC in a World Without Comparable Companies

Here’s where things get genuinely messy. Calculating WACC for crypto protocols requires comparables, but there aren’t clean ones. Is a DeFi lending protocol comparable to a bank, a fintech, or a software company? The answer is “kind of all three but not really any of them.”

We can start with a base rate for similar business models in traditional finance, then layer on crypto-specific risk premiums: premiums for regulatory uncertainty, technology risk , and market volatility.

The components:

-

Cost of equity: We can use CAPM, but beta estimation is problematic. Most crypto protocols don’t have public equity trading, so we can’t calculate historical beta.

-

Cost of debt: Most crypto companies don’t have traditional debt financing. When they do, it’s expensive.

-

Terminal Value: Where this breaks down is terminal value calculation. Assuming a perpetual growth rate for a protocol that might not exist in 10 years feels absurd. We can handle this by using multiple terminal value scenarios and probability-weigh these scenarios based on assessment of technology risk.

Worked Example

Let me walk through a simplified valuation of a hypothetical decentralized exchange to make this concrete.

Company Profile: “DexCo” operates a decentralized exchange generating revenue from trading fees. It holds million of its own governance tokens (DEXX) on the balance sheet, currently trading at $ per token. It also has $ million in cash. The company has employees, annual operating expenses of $ million, and generated $ million in protocol fees last year.

Step 1: Operating Business DCF

I forecast revenue using bottom-up assumptions. Current annual trading volume is $ billion with a fee rate.

| Year 0 | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | |

|---|---|---|---|---|---|---|

| Trading Volume ($B) | 2.0 | 2.4 | 3.0 | 3.9 | 5.1 | 6.4 |

| Volume Growth | — | +20% | +25% | +30% | +30% | +25% |

| Revenue ($M) | 8.0 | 7.2 | 9.0 | 11.7 | 15.3 | 19.2 |

| Operating Expenses ($M) | 5.0 | 5.5 | 6.0 | 6.5 | 7.0 | 7.5 |

| OpEx Growth | — | +10% | +9% | +8% | +8% | +7% |

| Free Cash Flow ($M) | 3.0 | 1.7 | 3.0 | 5.2 | 8.3 | 11.7 |

All figures in USD millions unless otherwise noted.

Operating expenses grow slower than revenue (economies of scale), driving margin expansion over the forecast period.

Using WACC of (reflecting high risk), terminal growth rate of :

- Present value of cash flows Years 1-5: $ million

- Terminal value (Year 5 perpetuity): $ $ million

- PV of terminal value: $M $ million

Operating business value: $50.9 million

Step 2: Token Reserve Valuation

million DEXX tokens $ $ million at current market price

But I apply a liquidity discount because:

- The company can’t dump million tokens without crashing the price

- Tokens are subject to vesting schedules

- Regulatory uncertainty about token sales

Token reserve value: $ million

Step 3: Sum-of-the-Parts

- Cash: $ million

- Operating business: $ million

- Token reserves: $ million

Total enterprise value: $110.9 million

Now, here’s where reality gets interesting. If DexCo’s equity is trading in secondary markets at $ million, we’ve identified a potential discount to intrinsic value. The questions become: Why does this discount exist? Liquidity? Information asymmetry? Fundamental disagreement about growth assumptions? Or are my DCF assumptions too optimistic?

The Hard Parts: Regulatory Risk, Technology Obsolescence, and Token Economic Drift

Even with a solid DCF framework, three major risks can blow up our valuation overnight.

-

Regulatory risk is the most immediate. The SEC’s approach to crypto regulation remains unclear despite recent developments. The regulatory landscape could shift dramatically with changes in SEC leadership or new legislation.

-

Technology obsolescence is the second killer. Sushiswap dominated in 2020-2021; by 2023, it had lost market share to newer protocols with better features. The half-life of competitive advantage in crypto is measured in quarters, not decades. The pace of innovation is too fast, the barriers to entry too low. A protocol that dominates today can be forked and improved tomorrow.

-

Tokenomic drift is the third and most insidious risk. Many protocols launch with governance tokens that don’t capture value: they’re purely for voting rights, with no cash flow entitlement. Then communities debate whether to implement “value accrual” mechanisms (fee sharing with token holders, buybacks, token burning). These debates can drag on for years, and outcomes are unpredictable.

When DCF Breaks Down Completely: Acknowledging the Limits

When this entire framework falls apart:

-

Pure speculation tokens: If a token has no underlying revenue, no product, no users—just hype and memes, DCF doesn’t apply. You can’t discount cash flows that don’t exist and never will. Dogecoin has a $ billion market cap and generates zero revenue. That’s not a DCF valuation gap; it’s a fundamentally different asset class.

-

NFT projects: Most NFT projects generate revenue through initial sales and royalties, but the business model is closer to art dealing than protocol economics. We’re valuing the creator’s ability to maintain cultural relevance and scarcity premium. DCF can value the operating company (if there is one), but it can’t value the NFTs themselves, which derive value from aesthetics, community, and social signaling.

-

Governance-only tokens with no revenue mechanism: As I mentioned with

UNI, if a token provides governance rights but no cash flows, DCF gives you a value of zero. The market clearly disagrees:UNItrades at $ billion market cap. That $ billion represents the market’s assessment of: (1) probability of future value accrual mechanisms being implemented, (2) value of controlling protocol treasury and parameters, (3) pure speculation. -

Protocols in rapid experimentation phase: If a protocol is still figuring out its business model, launching new products every quarter, pivoting between strategies, the DCF is essentially worthless.

Key Takeaways

-

DCF works for crypto—with a mental model flip. The underlying cash flow logic holds perfectly for fee-generating protocols. What breaks down is traditional capital structure assumptions, not the methodology itself.

-

Token reserves are assets, not treasury stock. Unlike traditional treasury shares that reduce equity, company-held tokens appear on the balance sheet as genuine assets because they derive value from network effects, not claims on corporate cash flows.

-

Value the equity, not the token. These are distinct instruments: token value comes from network utility and user demand; equity value represents ownership of cash, IP, and token reserves. The causation runs from network adoption to token value, to company asset value.

-

Use Sum-of-the-Parts (SOTP) valuation. Break the company into three buckets: cash and equivalents, operating business (core DCF), and token reserves (marked to fair value with liquidity discounts). This reveals potential mispricings hidden in blended valuations.

-

Crypto revenue models translate directly to TradFi analogues. Transaction fees Volume Fee Rate. For Lending protocols TVL Utilization Interest Rate Protocol Take. The forecasting mechanics are familiar; the adoption dynamics are the challenge.

-

Three risks can blow up your valuation overnight. Regulatory uncertainty (SEC), technology obsolescence (competitive advantage measured in quarters), and tokenomic drift (unpredictable value accrual mechanisms) require explicit scenario modeling.

-

Know when to put down the spreadsheet. DCF breaks down completely for pure speculation tokens, NFT projects, governance-only tokens without revenue mechanisms, and protocols still experimenting with their business model.